Introduction

Starting a business is a significant undertaking. But it’s simply the first of many. Most significantly, you will determine the legal structure of your company. A corporation is one of the most common options, alongside sole proprietorship, partnership, and limited liability company (LLC).

Corporations have several distinct benefits over other types of business structures. To begin with, unlike partnerships and sole proprietorships, the owners are not personally accountable for the firm’s obligations. A corporation is also ideal if you intend to develop your business to a significant scale.

However, deciding to incorporate is only part of the process. Entrepreneurs must also choose what type of organization they want to form. S Corporation vs C Corporation derives their names from the applicable provision of the Internal Revenue Code that determines how they are taxed. There is, however, more than a single-letter difference between them. This post will give you basic knowledge of S corporation vs C corporation.

C corporation and S corporation Defined

Corporation basics

A corporation is a business entity created by drafting articles of incorporation and filing registration paperwork with the state.

Shareholders are the owners of a corporation, and they elect directors to supervise corporate operations. The directors appoint executives to oversee day-to-day operations. Profits, known as dividends, are given to shareholders in proportion to the number of shares they possess.

A corporation is formed under state law and is legally distinct from its owners, which means that stockholders are not personally liable for the firm’s debts (liability for shareholders is limited to their investment in the business). Corporate debts apply only to the corporation’s assets. With a few exceptions, a shareholder is not personally accountable for company debts, and their assets are safeguarded from business creditors. Corporations must follow legal rules and “corporate formalities” that other enterprises do not.

Corporations must issue stock, create bylaws, have annual director and shareholder meetings, keep meeting minutes, the issue is written corporate resolutions for significant decisions, yearly file reports with the state government, and pay annual fees. Failure to do so may result in the loss of personal liability protection as well as the dissolution of the corporation.

C Corp and S Corp are tax classes offered to corporations and limited liability entities (LLCs). Corporations are taxed as C Corp by default. However, some can decide to be taxed as S Corp instead. LLCs are usually treated as sole proprietorships or partnerships, although they can also be taxed as C Corporations or S Corporations.

The Basics of C-Corpations

A C Corporation, is a legal company owned by shareholders. These shareholders elect a board of directors, which selects the management team because there are no restrictions on who can own shares in a C Corporation, it is preferable. A C Corp can be held by other firms and entities inside and outside the United States. There are no restrictions on the overall number of stockholders. A C-corporation also provides its owners with limited liability protection. If the company incurs debt or is sued, the owners are not held personally liable, and their assets are not in danger. A lender or a litigator might pursue the company as a whole rather than the individual owners.

The IRS taxes a C Corp for its business profits, which means its owners must also pay tax on personal income at the individual level for any dividend or stock sale gains. This structure is known as “double taxation” since dividends are taxed at corporate and individual levels. A firm can avoid double taxation by forming a limited liability company (LLC) or applying for S-corporation status. Still, it will be subject to additional limitations, such as the number of shareholders it can have. C Corp shareholders cannot deduct business losses from their income tax returns.

The Basics of S Corpation

An S Corporation is a business entity that falls under Subchapter S of the Internal Revenue Code. It is sometimes known as a “small business corporation” because it combines an LLC’s liability protection with a C Corp’s corporate-level standing.

An S Corp’s most significant distinguishing feature is its so-called “pass-through” tax structure. S Corp is not subject to the federal corporate income tax; dividend income is taxed exclusively at the individual level. This also means that if shareholders fulfil specific requirements, corporate losses might be compensated by revenue from other sources. S Corp gets the same liability protection afforded by corporation status as a distinct entity.

Various stringent requirements for operating as an S Corp might disqualify or disincentivize a company that would otherwise seek the status. S-firms are limited to 100 stockholders, cutting out corporations seeking to become public. The primary owners are citizens or permanent residents of the United States and certain domestic trusts, estates, and tax-exempt organizations.

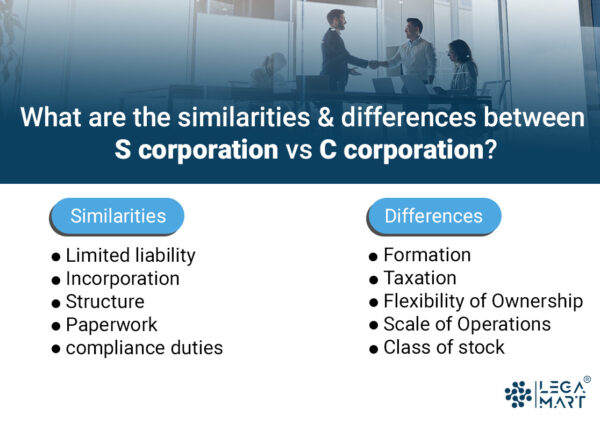

What are the similarities between S corporation vs C corporation?

S Corp vs C Corp is similar in several ways.

- Limited liability: Because S Corp vs C Corp is legally distinct from their owners, their shareholders have limited liability protection. Stockholders are not individually accountable for the company’s debts or commitments. This is a significant selling feature for a company.

- Incorporation: You must complete the necessary incorporation forms, file articles of incorporation, designate a registered agent, and draft company bylaws.

- Structure: While shareholders of an S Corporation or C Corporation control the company, they do not make the majority of the decisions. The company’s board makes management and policy decisions of directors, which shareholders choose. And the corporation’s officials—such as the CEO, COO, and CTO—are in charge of the firm’s day-to-day operations.

- Paperwork and compliance duties: S Corp and C Corp must fulfil specific documentation and compliance obligations, including issuing stock, paying fees, and conducting shareholder and director meetings.

What are the differences between S corporation vs C corporation?

While there are similarities between S Corp vs C Corp, there are also some stark differences.

Formation

| C Corp formation | S Corp formation |

| The C Corporation is the most common kind of corporation. When you submit articles of incorporation with your secretary of state to register your firm as a corporation, it will become a normal C corporation | Fill out IRS Form 2553 to organize your business as an S-Corp for federal tax reasons. To be classified as an S Corp for state taxes, you may need to complete extra paperwork at the state level. |

Taxation

| S Corp | C Corp |

| For tax purposes, an S Corp is a pass-through organisation, which means that shareholders record their portion of the business’s revenue and losses on their tax returns by submitting Form 1120S. All firm profits are allocated to the owners, who are subsequently subject to personal income tax. It is similar to the structure of a single proprietorship or a partnership. An S company cannot deduct the cost of fringe benefits provided. Thus they are added to the taxable income of all shareholders owning more than 2% of the shares. Furthermore, S Corporation and other pass-through entity owners (such as LLCs, sole proprietorships, and partnerships) may be eligible to deduct up to 20% of qualifying company income on their tax returns. Businesses in specialised service trades or professions, such as consulting, medical, or law, may encounter deduction restrictions at high-income levels. An S corporation may save owners money on taxes, though that isn’t always the case. | The Internal Revenue Service of the United States treats a conventional C Corporation as a separate legal entity (IRS). Profits made by the company are subject to corporate income tax. Shareholders must pay personal income tax on income gained from the firm, i.e. earnings paid out in dividends. This is sometimes referred to as “double taxes.” In other words, when the C-Corp files its corporate income tax return, it first pays taxes on its profits (Form 1120). If the business distributes earnings to shareholders in dividends, the C-Corp owners may have to pay taxes on those gains again on their income tax returns. Certain fringe benefits provided for employee welfare, such as healthcare and life insurance, are deductible from corporate profits, which helps reduce the corporation’s tax burden. The only way to avoid double taxation is to either not earn any profits (i.e., run at a loss) or reinvest profits back into the firm rather than issuing dividends. Wages and wages are generally deductible, including those paid to the owner. However, the IRS has the authority to “re-label” exorbitant salaries as taxable. |

Certain business-level tax deductions, such as charitable donations and fringe benefits, are fully deductible only for a C Corporation. A qualified accountant or business attorney can help you figure out the structure friendliest to your bottom line. More simply, you can visit the LegaMart directory and employ a lawyer to grasp all the details you need regarding the S corporation vs C corporation based on your questions from your smartphone.

Flexibility of Ownership

Although an S corporation may save owners money on taxes, this is not always the case. Certain business-level tax deductions, such as charitable contributions and fringe perks, are only completely deductible for a C Corporation. A knowledgeable accountant or company attorney can assist you in determining the structure that is most beneficial to your bottom line.

An S-owners Corp must be an individual, trust, estate, or non-profit. Certain businesses, such as banks and insurance firms, cannot have S status. C companies, on the other hand, can have unlimited stockholders. Any organization type, including institutional investors such as a mutual fund or a venture capital company, can invest in a C corporation.

The shareholders’ voting rights can be separated to implement alternative profit-sharing systems. A concept like this is ideal for organizations looking to acquire cash through sophisticated vehicles like initial public offerings (IPOs).

Scale of Operations

The S Corp classification is better suited to smaller or new businesses that seek to avoid the double taxation effect of the C Corp structure. Most new enterprises anticipate losing money in their first few years. The S structure is especially advantageous since it allows owners to balance their other income with the losses above, lowering their overall tax obligation.

Some states do not recognize S status, and while converted firms are recognized by federal law, they may still be taxed under the C status structure. Before switching between corporate formats, it is necessary to perform extensive study on area legislation.

Class of stock

An S Corp can only issue one type of common stock. On the other hand, a C-corporation can give many kinds of stock, such as Class A, Class B, ordinary, and preferred shares.

Choosing between S corporation vs C corporation

There is no alternative for legal and tax guidance. Still, an overview of the advantages and downsides may steer a company on the correct path and assist its owners in asking the right questions about founding a corporation or electing corporate status.

S Corp Pros and Cons

| S Corp Advantages | S Corp Disadvantages |

| Directors, officers, stockholders, and employees have limited responsibility. | Maximum limit of 100 shareholders. |

| Pass-through taxes avoids the double taxation of C Corporations. | Only US citizens, permanent residents, and certain domestic trusts, estates, and tax-exempt organizations are permitted to hold shares under strict shareholder restrictions. Partnerships and companies are not allowed to own S Corp shares. |

| In some situations, corporate losses might be passed on to owners. | You can only have one class of stock. |

| Like a C Corp, it has a separate existence from its stockholders, which means it may continue to operate even if major shareholders leave. | Harder to raise equity financing than C corporation |

| File taxes annually instead of quarterly. | More IRS scrutiny, particularly about the balance of wage payments against profits. |

| This might result in a cheaper self-employment tax for LLC owners who choose S Corp status. | Corporations have a more rigid structure and need more money and effort to manage than other company formations. |

C Corp Pros and Cons

| C Corporation Advantages | C Corporation Disadvantages |

| All workers, shareholders, directors, and officials have limited responsibility. | Earnings and realized gains are taxed twice: first under a business income tax and then again as personal income for shareholders. |

| No restrictions on the number of allowed shareholders. | No personal write-offs mean shareholders cannot deduct business losses from their personal income tax returns, as some S Corp shareholders and members of other corporate forms may. |

| There are no restrictions on stockholders’ countries of origin or business status. | Corporations have a more rigid structure and need more money and effort to manage than other company formations. |

| Equity funding is easier to get than in the case of an S corporation or other business structure. | |

| Can issue more than one class of stock. | |

| The lower maximum tax rate than the total personal tax rate applies to S corporations, sole proprietorships, and partnerships. |

Conclusion

No optimal option exists among the various business formats and tax regimes available. Choices for incorporation or business registration should be based on the unique circumstances of each firm, and owners should consult with legal and tax specialists throughout the business formation process. Regardless, it is critical to be aware of the possibilities available and remember that many organizations shift from one structure to the next as they develop.

Now that you understand the distinctions between S corporation vs C corporation and its benefits and drawbacks, you’re well prepared to make an informed decision for your company. Many small firms can save money on taxes by forming an S corporation, but C corporations provide additional possibilities for expanding and raising capital.

How you organize your business is a massive choice with significant consequences for your company’s future. Consult with our business lawyer or accountant if unsure about selecting a business entity or properly organizing your firm.