- What is a Business transaction?

- Benefits of recording Business Transactions

- What are the various types of Business Transactions?

- Examples of Business Transactions

- Characteristics of a business transaction

- Steps of a Business Transaction Analysis

- Business Transactions vs. Investment Transactions

- Get Help with a Business Transaction

- Frequently Asked Questions

“Where there is no accountability, there will also be no responsibility.”

― Sunday Adelaja

A transaction must first be understood to understand what a business transaction is. An exchange of goods, services, or money for commercial or non-commercial purposes is recorded as a transaction. Because they provide an abstract perspective of the interactions among firms to achieve a business goal, business transactions are becoming increasingly significant. Technically, the growth and future of a business are based on the transactions that make up that growth.

What is a Business transaction?

A business transaction is an interaction in the real world where something is exchanged, typically between an enterprise and a person or another enterprise. For instance, it might entail exchanging cash, goods, knowledge, or service requests. To keep track of what happened, some bookkeeping is typically needed. Due to its greater scalability, dependability, and affordability, computers are frequently used to perform this bookkeeping. Communications between the parties to the business transaction are frequently conducted over a computer network, like the Internet. Transaction processing (TP) is the act of processing business transactions through a network of computers.

Business Transaction processing systems must handle high volumes effectively, avoid errors brought on by concurrent operation, avoid producing partial results, grow incrementally, avoid downtime, never lose results, offer geographical distribution, be customizable, scale up gracefully, and be simple to manage.

The following characteristics must be present for a transaction to be classified as a business one. Business transactions can be as simple as a cash purchase or as complicated as a long-term service contract.

- Money can be used to quantify the transaction.

- The business and the third party conduct the transaction.

- The deal is being made on behalf of the company, not for a person.

- Authorized legal records, such as an invoice, sale orders, receipts, etc., are used to record the transaction, which backs the transaction.

A business transaction can occur between two parties working toward common goals or between a company and a client, like a retailer and a customer who buys something in the store.

Most businesses typically use five different business accounts to accurately record all business transactions:

- Assets

- Liabilities

- Equity

- Expenses

- Revenues

These business accounts, when analyzed and contrasted, can give us a good idea about how financially sound a company is.

Benefits of recording Business Transactions

- Assists in segregating the income generated from business operations from other sources, such as capital gains, lottery income, salary income, etc., that may be combined.

- Assists in assessing the efficiency of the organization’s operations and its ability to generate profits over the given period.

- It enables the assessee to maintain accurate records and file their income tax returns in compliance with statutory regulations by properly categorizing their income and expenses into the appropriate categories.

- Maintaining records of transactions enables timely preparation of financial statements for tax returns, thus helping meet deadlines and avoiding penalties.

What are the various types of Business Transactions?

The two different types of business transactions in accounting are listed below.

- Cash Transactions and Credit Transactions

- Internal Transactions and External Transactions

Cash Transactions and Credit Transactions

A cash transaction is one where the payment was made or received in cash at the time of the transaction, as indicated by the label “cash transaction.”. An illustration of a cash transaction would be if Mary purchases a new shirt from a store and pays at the register. Even though the payment was made with a debit or credit card, this transaction is still regarded as a cash transaction because it was made at the time it took place.

Payment in a credit transaction is made after a predetermined period, also known as the credit period, like Mary, who wants to purchase a couch from a furniture store. The shop accepts payments up to 30 days after the sale rather than at the time of purchase. Mary will be required to pay for the couch once the 30-day credit period has passed, even though no money is exchanged at the time of the sale.

Internal Transactions and External Transactions

Internal transactions, also known as “non-transactions”, occur when no outside parties are involved. These transactions don’t involve the exchange of values between the parties, but the event that includes the transaction is monetary and affects the company’s financial health. The recording of fixed asset depreciation and the recognition of the loss of assets lost to fire, among other things, are examples of internal transactions.

When a business exchanges money for goods or services from outside parties, these exchanges are referred to as external transactions (also known as exchange transactions). The term “external transaction” describes any transaction that isn’t internal. These are the typical transactions that a business makes every day. Examples of external transactions include purchasing goods from suppliers, selling goods to customers, buying fixed assets for the business, paying rent to the owner, paying utilities like gas or electricity, paying employees’ salaries, etc. A large portion of all business transactions involves external transactions.

Examples of Business Transactions

- Purchasing insurance from an insurer.

- Purchasing stock from a vendor.

- Selling products to a customer in exchange for money.

- Providing a customer with goods on credit.

- Wage payments to workers.

- Taking out a loan with a lender.

- Selling stock to a buyer.

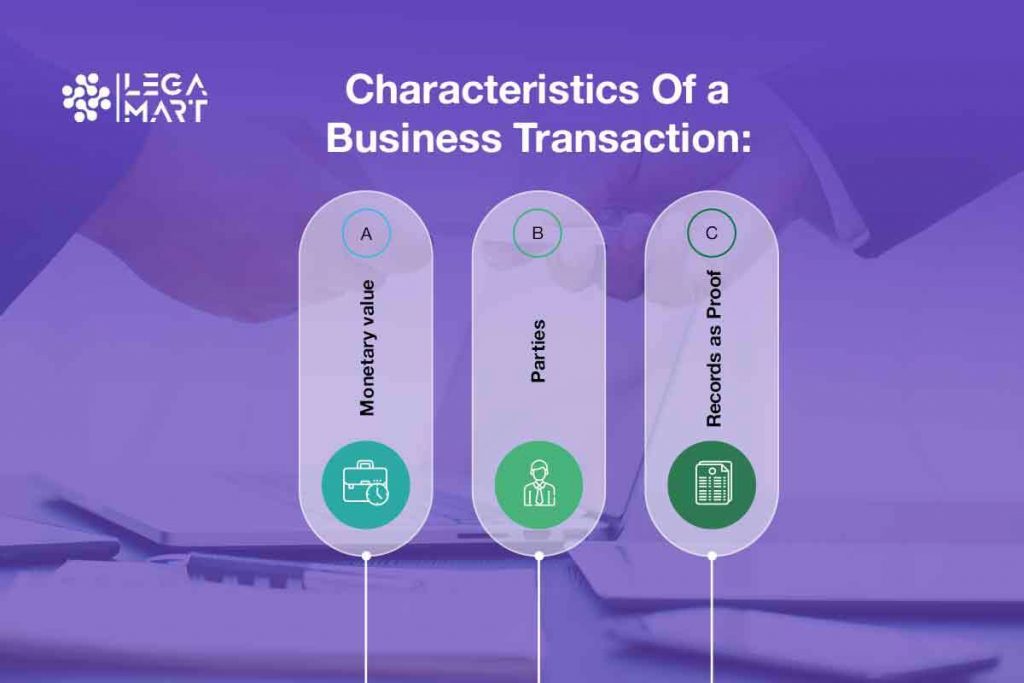

Characteristics of a business transaction

A business transaction must have several essential characteristics to be categorized as an economic event. The following are these characteristics:

Monetary Value

It must be worth the money. The company’s finances must be impacted by the event. There are two ways to view this effect: qualitatively and quantitatively. When the company’s assets or liabilities change, a quantitative change occurs. When a company’s assets and liabilities remain unchanged but its financial situation changes, this is called qualitative change. It indicates the non-material effects of transactions.

Parties

For an event to qualify as a business transaction, two or more parties must be involved. Further, the role must be carried out on behalf of the business.

Records as Proof

Documentary evidence, such as an invoice or memo, should support the occurrence. A voucher or source document is the record that attests to the event. Some economic occurrences can’t be categorized as business transactions that take place during the normal course of a business. If an event could be added to an accounting record, that is the simplest way to determine whether or not it is a business transaction. If it cannot be added, it is most likely not a business transaction.

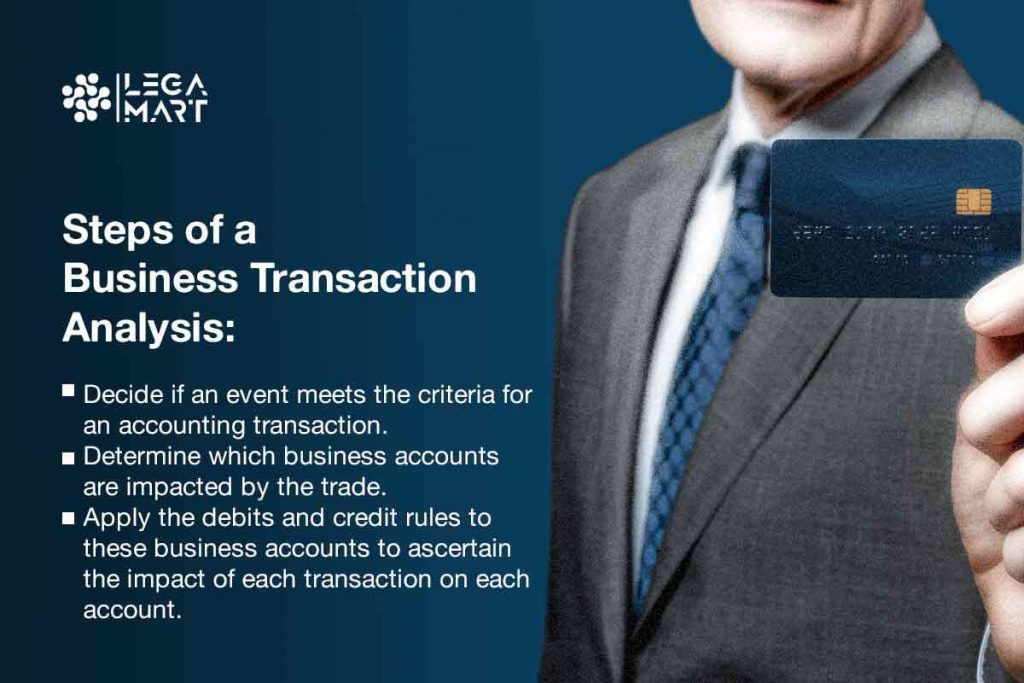

Steps of a Business Transaction Analysis

Accounting transaction analysis, the first step in the process, entails examining each transaction that impacts your company. A transaction is any occurrence or activity that affects your company’s finances economically. You can determine how each economic event affects the accounting equation, which must remain in balance after each transaction has been recorded, by analyzing each economic event.

You can accurately record each transaction in your accounting books by identifying and analyzing how it impacts the owner’s equity and different assets and liabilities. Although it may seem like a difficult process, once you break it down into its parts, it becomes clearer.

You must first comprehend what the accounting equation is and how it functions to fully comprehend how accounting transaction analysis affects the fundamental accounting equation.

Assets = Liabilities + equity is the fundamental accounting formula.

Your company’s financial transactions must be categorized into the correct asset, liability, and net worth categories.

Assets are everything that your company owns, including money, machinery, property, buildings, land, inventory, and business bank accounts receivable.

Any debt your company owes, including mortgages, loans, long-term debts, notes payable, and other accounts payable, is a liability.

Net worth, referred to as equity in the accounting equation, is essentially net assets or what would be left over after paying off all of your company’s debts.

For a sole proprietorship, partnership, or corporation, equity is denoted as owner’s equity, Partner’s equity, Stockholder’s equity, or Shareholder’s equity. Equity is divided into two parts: Revenues and Expenses, in the expanded accounting equation. Rent, utilities, payroll, and taxes are just a few examples of the costs incurred in generating revenue, which is what the company makes by selling its products or services.

Your business needs to balance its assets and liabilities to operate effectively. When you examine an accounting transaction, you’re figuring out how it changes the fundamental accounting equation. The balance sheet of your business must always show a balance between the two sides of this equation.

You track the sources and destinations of your company’s funds using double-entry bookkeeping. As the name suggests, this procedure involves both a debit and a credit and involves two entries.

Debits raise assets for your business, lower revenue accounts, lower liability or equity accounts, and raise expense accounts.

Credits reduce the assets of your business while increasing the revenue, liability, or equity accounts and decreasing the expense accounts.

As you can see, debits and credits contradict one another. Since there is a credit for every debit when using the double-entry method, and vice versa, there will always be a credit for every debit. This maintains the balance of your accounting equation, so you are aware that if it is out of balance, your bookkeeping is incorrect. When creating your financial statements, you’ll use the data produced by these entries. These assertions provide information about your company’s profitability and suggest future financial priorities.

Your business makes purchases or sales, takes out credit or extends credit to others, generates income, or incurs expenses. These are all actions that come from conducting business or transactions. Each of these transactions modifies one of the three components of the fundamental accounting equation, but only if it affects your business financially. Before you can record an event, it must first be thoroughly examined to determine whether it falls under a transaction category. This procedure includes the following steps, among others:

Step 1: Decide if an event meets the criteria for an accounting transaction. For instance, if you sign a lease on a new building, there isn’t an accounting transaction because no money was exchanged and no money was involved. However, if you paid a deposit when you signed this lease, that deposit counts as an accounting transaction because there was a money exchange that needed to be recorded.

Step 2: Determine which business accounts are impacted by the trade. Asset accounts are increased by debits, while credits decrease them. The liability of the business account is increased by credits and decreased by debits. For instance, your business purchases new inventory worth $10,0000 on credit. Inventory is listed under assets, while the outstanding balance is listed as an account payable under liabilities. Several business accounts that are frequently used comprise

Asset Accounts: Cash, receivables (including notes and bank accounts), inventory, prepaid expenses, real estate, buildings, and equipment.

Accounts for liabilities include accrued liabilities, payable notes, and bank accounts payable.

Common stock, retained earnings, dividends, revenue, and expenses are all included in owner/stockholder equity accounts.

Illustration

Because your business purchased new inventory, the Inventory Account under Assets increases by $10,0000.

Due to an increase in your company’s debts, the Accounts Payable Account under Liabilities is increased by $10,0000.

Liabilities are credited, and Assets are debited, so the balance for this transaction is maintained.

Always check your invoices and receipts to ensure you enter the correct transaction amount for each account. In such a case, even if your entries are accurate, your bank statement won’t agree with your financial reports.

Step 3: Apply the debits and credit rules to these business accounts to ascertain the impact of each transaction on each account. To keep the accounting equation balanced, each transaction needs at least two related but opposing accounts. This means that each transaction must debit at least one account and credit at least one account in an equal amount.

Business Transactions vs. Investment Transactions

- Business transactions refer to transactions carried out by any business involving trade, commerce, or manufacturing. On the other hand, investment transactions involve buying or selling marketable securities and other assets that may or may not be directly related to the organization’s core operations.

- Business transactions frequently occur in large numbers as they are part of the organization’s regular operations, while investment transactions are independent and entered into less frequently.

- If buying and selling an asset is integral to the assessee’s regular trading business, such transactions will be treated as business transactions. However, if buying and selling an asset is an independent activity outside the ordinary business course, these transactions will be classified as investment transactions.

- Income from business transactions is considered the organization’s income. It is subject to taxation under the “Profit and Gain from Business Property.” In contrast, income from investment transactions is treated as capital gain and taxed under the category “Income from Capital Gains.”

Get Help with a Business Transaction

Business transactions are those that the assessee enters with a third party for business purposes, are valued at money, and are noted in the assessee’s accounting records. The documentation of the event, which provides adequate support for the transactions, is required for the recording of these transactions into the assessee’s books of accounts. The assessor can evaluate his business income separately from other incomes through business transaction recording. The assessee can file his income tax returns (ITR) for the necessary period thanks to the bifurcation, which complies with all legal requirements.

Navigate the complexities of business transactions confidently with LegaMart. Our network of seasoned legal experts is ready to guide you through every step, ensuring compliance and strategic success. From start-ups to established enterprises, we provide the insights and tools to make informed decisions safeguarding your financial health. Join LegaMart now and transform your business transactions into strategic advantages for growth and stability. Start your journey with LegaMart today – your partner in business finance expertise.

Frequently Asked Questions

What is a Business Transaction, and How Does It Differ from Ordinary Transactions?

A business transaction is a financial event that involves an exchange of value (such as goods, services, or money) between a business and an individual or another business. It is distinct from ordinary transactions in that they are typically conducted for commercial purposes and involve legal documentation like invoices, sale orders, and receipts. Examples include purchasing stock from a vendor, selling products to a customer, or paying employees. The key aspect of a business transaction is that it affects the financial position of a business and is recorded in its accounting system.

What are the Different Types of Business Transactions and Their Importance?

There are two main types of business transactions in accounting: Cash Transactions and Credit Transactions, as well as Internal and External Transactions.

Cash Transactions involve immediate payment, such as buying a shirt with cash or a card.

Credit Transactions involve deferred payment, like buying a couch on a 30-day payment term.

Internal Transactions affect the company’s financial health but do not involve external parties, like asset depreciation.

External Transactions involve exchanges with outside parties, like purchasing goods or paying salaries. These transactions are crucial as they form the backbone of a company’s financial records, impacting everything from profit measurement to tax compliance.