- Introduction

- What is a Joint Venture?

- Types of Joint Ventures

- Differences between domestic and cross-border joint ventures

- What is a Joint Venture Tax?

- How is Joint Venture Income Taxed?

- What are the Tax Considerations When Structuring a Joint Venture?

- What are the Tax Implications for a Joint Venture?

- Are Joint Ventures Double Taxed? How can you avoid it?

- Conclusion

- Frequently Asked Questions (FAQs)

Introduction

As an exception to all the fascinating things that happen only once in life, double taxation in joint ventures can certainly happen twice. For any entrepreneur who owns a successful business, the last thing he may want is to get taxed on his income more than once.

Any organisation collaborating with another company seeks to expand its reach and presence in fields where it cannot do it independently. As the companies collaborate to make profits, no company would like to pay joint venture tax twice, as it would discourage the companies from collaborating and hinder their growth and partnership.

The concept of double taxation in joint ventures refers to when a company pays taxes on its gains, and its shareholders pay personal taxes on dividends or capital gains from the company. This article aims to explain the basics of double taxation in joint venture agreements and answer the key question: How to avoid double taxation in joint ventures?

What is a Joint Venture?

A joint venture (JV) is a commercially arrangement between two or more independent parties (referred to as joint venture parties) to do something specific.

E.g., to develop and market a new product, where the two (or more) parties can achieve their aim better together than separately like one may have the assets to manufacturing capacity and the other may be competent in research to develop something useful. Their collaboration will lead to significant development.

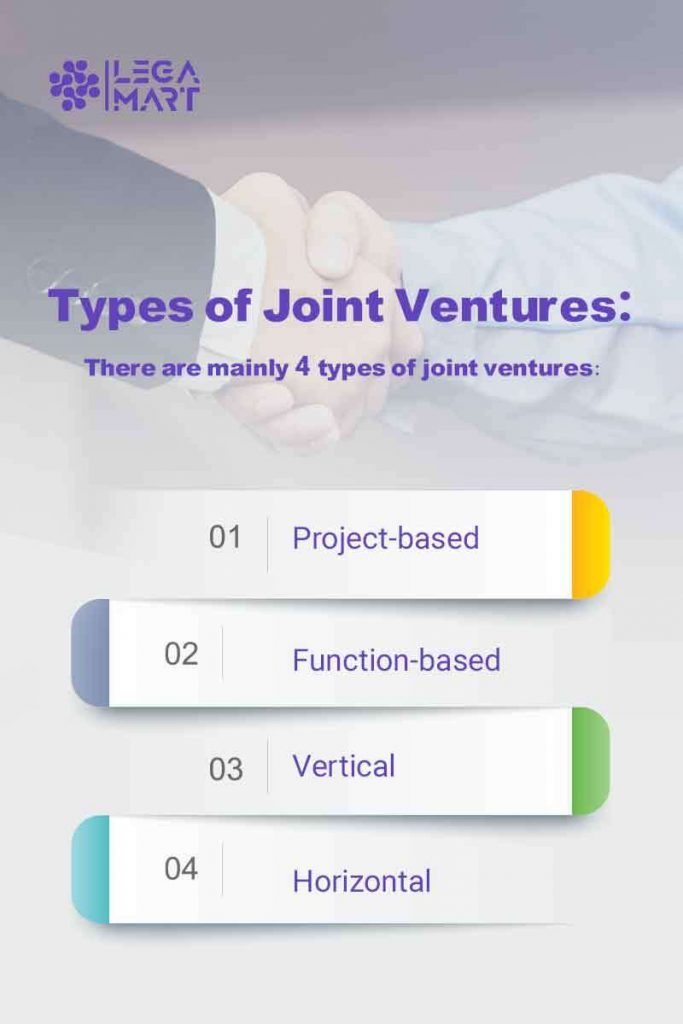

Types of Joint Ventures

There are mainly 4 types of joint ventures:

- Project-based Joint Venture. Within this JV, the partners come together to accomplish a fixed task. Considering that the collaborations, in this case, are done for an exclusive purpose, the collaboration ceases to exist once the task has been accomplished.

- Function-based Joint Venture. Within this JV, the parties form a mutually beneficial arrangement wherein the parties gain from each other’s expertise in different areas. This helps the parties to perform efficiently and effectively. It is important to consider and be sure that the would-be partner companies would be able to function effectively and perform together efficiently.

- Vertical Joint Venture. Within this JV, the transaction is between the buyers and the suppliers. This is often also termed bilateral trading. Here, different manufacturing stages of the same product are integrated, creating economies of scale to reduce the per-unit cost of the finished product. This type of joint venture has a history of being highly successful and has also resulted in forming a good relationship between the buyer and the supplier.

- Horizontal Joint Venture. Within this JV, the companies that are selling or dealing in similar products and who are direct competitors in the market end up joining hands to create an output that can reach the customers of either party. This type of JV is often prone to disputes, considering that both companies are involved in similar businesses.

Differences between domestic and cross-border joint ventures

Over and above all the legal and tax considerations for domestic joint ventures, additional issues are raised through cross-border joint ventures. This is because such JVs involve parties from different legal and tax considerations and with different conduct of business across international borders. Some of the issues experienced are:

- The possibility of locating the JV in different jurisdictions

- The possibility of using different legal vehicles in diverse jurisdictions

- Restrictions on foreign investment, ownership, and control, depending upon your country-specific laws

- The ‘overriding’ concepts of local laws are capable of rendering the provisions of the agreement void or unenforceable.

- Ensuring that fiscal transparency and neutrality are maintained across borders.

- The overseas employment of employees from the JV’s participating companies.

- Need to choose the appropriate law and forum for the resolution of disputes.

To know more about joint ventures, refer to:

Joint Venture Termination Agreement: How to end and what happens after Termination?

Joint Ventures: Do they need Insurance, and if so, why?

What is a joint venture tax?

Now that we know how joint ventures work, let’s address the elephant in the room. Taxes. Any businessman in the right mind will raise this question first; How are joint ventures taxed? In initiating a joint venture, the most standard task the two players can undertake is to set up a new entity.

The business arrangement between the two players will help determine how taxes are handled. The joint venture will have to pay taxes as any other business or corporation if it is a separate entity. If it operates as a Limited Liability Company (LLC), its profits and losses will pass to the owners’ individual tax returns like any other LLC.

Within most JV deals, tax considerations play a key role in deciding the following:

- The choice of joint venture vehicle

- Where will it be based

- The manner in which the joint venture shall be terminated and operated

While it might not be identical, similar tax issues shall arise in any proposed cross-border joint venture structure. Therefore, the tax advisors should be involved at the earliest stages of the structuring process to identify potential tax problems and promptly offer solutions.

How is joint venture income taxed?

Double taxation in joint venture agreements is one of the essential tax principles involved in joint ventures that discusses income taxes disbursed double on the exact origin of income. It takes place when earnings are taxed at the corporate level as well as at the individual level.

Double taxation in joint ventures also emerges in international trade, where the exact income is subject to taxation in two countries.

Any chargeable gain made by such shareholders may result in a tax liability on the disposal of an asset to the JV company and the disposal of a shareholder of any trading stock, transfer tax, or VAT liability.

Setting up

In most JVs, the parties contribute their assets (with the possibility of including shares in subsidiaries) to the JV. It becomes important to assess the tax cost of contributions, considering that they can sometimes make the formation of the JV extremely expensive. A variety of taxes may be relevant at this stage:

- Capital Gains Tax. This depends on the country where the asset is located, considering that it may be taxed on the difference between the asset’s acquisition cost and the JV’s disposal value.

- Transfer Tax. It is seen that most countries end up charging transfer duties on the sale of certain assets, such as shares and land. You might have to include a notarization fee separately as well.

- Transfer of assets might be subjected to Value Added Tax or similar indirect taxes.

- Jurisdictions like Switzerland charge a capital duty on the issue of shares. This becomes relevant for a JV if it decides to issue shares in consideration of the transfer of assets to it.

Operating

The following operational tax issues shall be invariably raised during most of the JV negotiations:

- Minimisation of tax in a joint venture vehicle.

- Avoiding any tax leakage on the distribution of profits or gains in the JV vehicle to the JV parties. This includes the avoidance of double taxation on any distribution.

- Obtaining relief for losses that a JV might sustain.

What are the tax considerations when structuring a joint venture?

One of the most important ideas behind arranging a joint venture is to make sure that it is set up tax-efficient to reduce any form of double taxation in joint ventures during filing on the gains made. Below are listed some of the fundamental principles that are necessary while structuring a qualified joint venture.

Extraction of Profits: A critical consideration for shareholders is how they can extract profits from the joint venture and the tax treatment of such receipts. The JV company will be subject to tax on its profits, so there will be leakage at the level of the JV company. Any such amounts must then be distributed to shareholders.

Transfer of Assets into the JV Company: Parties to a joint venture agreement transfer their assets into the joint venture to achieve their end goal; such transfer of assets and resources may lead to tax liabilities. When tax liabilities arise, these assets and resources should be identified earlier so that the tax liabilities can be calculated as part of the joint venture agreement and avoided later on.

Transfer Pricing: Some joint venture agreements deal with the continuous supply of goods or services by one or more of the shareholders to the JV company. In such a situation, transfer pricing rules can be evaluated and involved in the agreement.

Secondary Tax Liabilities: If needed in a situation, the joint venture agreement can include detailed requirements and conditions to ensure that the expense of resulting secondary tax liabilities will fall on the shoulders of the shareholder who was liable in the first place for such tax.

Tax Consolidation: As per the situation, before undertaking the joint venture agreement, a financial consultant can determine whether the joint venture company falls under a shareholder’s tax association by a matter of law or by-election (such as in the UK, a VAT group).

If such a situation persists, necessary provisions will have to be implemented to ensure that the resulting organisation is not subject to discrimination.

Management of Tax Affairs: It may be necessary to define the terms and conditions as to the commercial tax-related working of the joint venture organisation. Depending on the requirements, all these conditions must be assessed and outlined in the joint venture agreement.

What are the main tax issues associated with setting up the joint venture, transferring assets, and making payments?

Transfer of assets into the JV company

Shareholders who transfer assets into the Joint Venture business may be seen to have sold such assets, which could have possibly resulted in tax consequences. Transferring assets into a Joint Venture business may result in different tax liabilities. For instance:

- Any chargeable gains such shareholders make on selling an asset to the Joint Venture business may result in tax obligations.

- If a shareholder sells any trading stock, there may arise a tax obligation.

- If the shares of entities are transferred to the Joint Venture firm, a transfer tax liability (similar to stamp duty / stamp duty reserve tax in the UK) may also become due.

- If land is transferred to the Joint Venture business, a transfer tax (such as stamp duty land tax liability in the UK) may become due.

- If specific assets are transferred but do not represent a “transfer of a going concern,” a TGST liability may result.

The effects of such tax liabilities could be lessened using several potentially applicable reliefs. However, based on the particular facts and circumstances present during the proposed transfers, a detailed analysis of the availability of the pertinent relief(s) will be required. Additionally, if the shareholder has relevant losses that can be used to offset any profits or gains from the transfer of assets into the Joint Venture business, some of the direct tax liabilities may also be reduced.

Early identification of relevant assets to be transferred into the Joint Venture company will ensure that the tax treatment can be easily determined and factored into the economics of the transaction.

Making payments

- Withholding Taxes: This is applied depending upon the jurisdiction and payment type. Withholding taxes are applied to payments made to joint venture partners for their services, royalties, interest, or dividends.

- Thin Capitalization Rules: Some jurisdictions have certain laws restricting how much interest on loans from related parties can be deducted, which may also affect the joint venture’s financing plans.

- Gains/Losses from Foreign Exchange: When payments are made or received in foreign currencies, exchange rate variations may sometimes result in gains or losses that could have tax repercussions.

- Double taxation agreements: When it comes to cross-border transactions, agreements between nations regarding double taxation come into play and may impact the rates at which taxes are withheld from payments.

- The deductibility of interest payments is subject to restrictions in some jurisdictions, especially if they are made to organizations located in low-tax nations.

- Goods and Services Tax (GST) may also apply to payments made within the joint venture, depending on the payment type and jurisdiction.

You should remember that every scenario is different, and the tax consequences can also change depending on the countries involved in the transactions and treaties, the type of joint venture, and the precise assets and payments being transferred. We advise you to work closely with tax experts knowledgeable in domestic and foreign tax legislation to ensure compliance and optimize the tax structure.

Are joint ventures double taxed? How can you avoid it?

Joint ventures fall under taxation as an establishment or collaboration. Organisations taxable as corporations will be affected by double taxation in joint ventures, where both the corporate and the shareholder levels will be subject to the double tax. But not to worry, as a satisfactory solution is available right here!

Contractual Joint Venture: The ultimate solution would be to arrange a contractual joint venture where the parties involved do not set up any individual establishment to harbour the joint venture. Instead, the parties enter into contracts and make their profits and losses. They pay tax only on their profits. This joint venture can be valuable to parties who can bid for mega contracts by merging the resources. A critical benefit of dealing in contractual joint ventures is that there are no joint or separate penalties for the failures of the venture.

Conclusion

The question raised in the introduction was how to avoid double taxation in joint ventures. The answer is plain and straightforward.

Move to a contractual joint venture. But why such a hue and cry about it? Isn’t it better just to move forward with creating a joint venture agreement and getting the wheels started on the collaboration? It is where many organisations make mistakes. It is, therefore, essential to consider the tax position of both the JV company and the shareholders early in establishing the joint venture to ensure that the financial modelling accurately reflects the tax position of each shareholder.

For more valuable updates on double taxation in joint ventures, talk to a LegaMart corporate expert for tips on avoiding double taxation, and don’t forget to bookmark this page for future reference. Keep progressing and developing!

Frequently asked questions (FAQs)

How do tax considerations play a key role in Joint Ventures?

Within most JV deals, tax considerations play a key role in deciding the following:

- The choice of joint venture vehicle

- Where will it be based

- How it shall be operated and terminated

What are the types of tax considerations made while structuring a Joint Venture?

One of the most important ideas behind arranging a joint venture is to make sure that it is set up tax-efficient to reduce any form of double taxation in joint ventures during filing on the gains made. Below are listed some of the fundamental principles that are necessary while structuring a qualified joint venture.

- Extraction of Profits

- Transfer of Assets into the JV Company

- Transfer Pricing

- Secondary Tax Liabilities

- Tax Consolidation

- Management of Tax Affairs